|

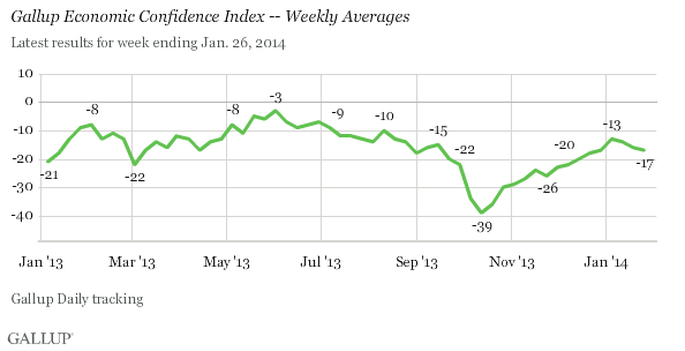

A, needed, pullback is gripping the equity markets. The SPX has lost roughly 3.5% of its value; accordingly, consumer confidence has slipped. “Strong household spending and robust exports kept the U.S. economy on solid ground in the fourth quarter, but stagnant wages could chip away some of the momentum in early 2014." January, is down almost 6% MTD and YTD. There is a known pattern; the year follows the first month of that years returns trend (body follows head, right?). The author thinks that given the positive data flow at the end of 2013, means that there is little chance that the equity markets in 2014 end negative. There is acceleration in employment, which means acceleration in consumption, money velocity etc.… Although it is possible for the year to end poorly (2014), the economy would to need grow at a blistering pace of < 3.2% for any reported number exceed the great growth we had in q3 of 2013.

This retracement is linked to emerging market counties, however, the underlying investment thesis has not changed. The countries did not change their trade partners nor did they reduce their rate of consumption. Rather, the currencies have decreased in value, their fundamentals have not changed. This could be a negative indicator, domestically if their currencies stay at this level, a depressed currency means that we, or other countries cannot sell tools they need to grow, thereby hurting our growth and growth of other countries. That could pose a serious problem for the global economy. Generally, global GDP is picking up. The auto industry is leading the way (probably led by China); building orders, construction and airlines (to name a few, but economically important) are seeing an increase in order flow/completed orders. Hoping we are experiencing a brief retracement, led by currencies of emerging markets. Optimistically, the trend will pick back up soon. With positive data coming from most countries, consequentially, order flow should increase among all industries, shipping products to various countries that have ordered them. This, in return should boost global gdp. The IMF last week forecast the emerging markets would grow at 5.1% this year, compared with 4.7% in 2013. China is expected to grow at 7.7% this year — hardly a crisis by anyone’s standards. Even hard-hit Turkey is expected to expand by 4% over the next twelve months. Too optimistic? Not really. The euro-zone has stabilized, at least for the time being, which will help Eastern Europe and Russia and Turkey. The U.S. is growing faster than at any time since the crash, which will help South America. So long as China can stay on course, it will carry on lifting the whole of Asia. Emerging Africa remains one of the fastest-growing regions in the world, and shows few signs of slowing down. -- Growth in emerging markets is accelerating, not slowing down. The recent selloff is blamed on EM countries, however, its completely normal to have an unprovoked sell off after 16 months of extraordinary returns. Link

Although their respective currencies have cheapened in the MINTS countries, their YoY GDP growth (year over year) of the South American, southern Africa, and southern Asian countries is impressive. The economy in Mexico, is growing very quickly. What could be a potential problematic point is that the Mexican Peso is highly correlated to South American currencies. This could be a problem for two reasons: 1) the recent retracement is blamed on currencies which is a major concern for growth due to the second reason, 2) without a strong currency they may not be able to properly or effectively develop their oil fields, those are a major key for growth. A large contributor to the Mexican economy is the economy of the US. Everyone knows that the move by the Fed to back off from asset purchases, and eventually to raise interest rates, will have major economic impacts here and abroad. The problem is in predicting what those will be and, especially, the magnitude of the effects. One source of uncertainty is the transition from a Bernanke Fed to a Yellen Fed, but it would be easy to over-estimate the importance of that factor. In reality, there is quite of lot of common ground between the outgoing and incoming Chairs. The more important issues revolve around the fact that we are simply in uncharted territory. The sturdy increase in demand should put the economy on a stronger growth path this year. However, anemic wage growth could take some edge off consumer spending early in the year. Given everything, the author thinks that this year should be in the black for equities. Going from a +30% year to a negative year, sequentially, is rather daft. As well, consumer spending rose at the fastest pace in 3 years despite the government, coincidentally (tapering) or reducing spending at the same time. The positive data flow is certainly laying the groundwork necessary for 2014 to be a positive year, again, not as great a rise as 2013 but still belying the impression that January has given the market.

0 Comments

The equity market seems to have lost steam (but hopefully not momentum) with the turn of the year, and especially in the second half of the month. Equities seem to be fair-valued—in this type of market fundamental analysis, AND having a longer time horizon for expected profits are keys to excess returns. With the recent pullback, it should create buying opportunities and will lure investors back into the market. Whereas all of 2013, especially the last quarter of 2012, was a “shooting gallery,” when it seemed like almost any equity you poured money into yielded awesome gains. This year it would be wise to look at historical price charts, and also look if order flow is increasing, which clearly points at higher net income. Earnings momentum, undoubtedly is an advantage to, all this coincides with the suggestion that fundamental analysis should be core to the equity selection process. Earnings momentum ended last year on a very positive note, q1 earnings should confirm reported earnings. A “great rotation” from equities into fixed income could come this year, as said GDP growth follows equity returns and equity returns. Moreover, with the increasing average age of the population, there is a high chance this shift could happen within >10 years. It would be shrewd to look for counties that this shift will happen sooner rather than later.

A pullback after the relentless rise we experienced , unbroken for <12 months), is more than needed, corrections serve two purposes. They help to slowly restore faith in the equity market by: pulling investors who remained on the sidelines after the tremendous run of last year into the market and with more investors participating the swing to positive territory could be much more dramatic. The beginnings of this trend were apparent at the beginning of this year, likely due to the volatile beginning of the year. Also, it gives a chance for investors already in the market to rebalance or adjust weightings without too big of a hit on year-to-date returns. Thankfully this correction happened towards the beginning of the year. Pent-up profit taking was apparent in the beginning of this year; many investors were probably delaying profit taking for tax reasons. Such tax strategies are positive for personal wealth, but deleterious for the market and popular equities (making them more attractive). The volatility of the beginning of the year is also a positive for investors coming off the sidelines, and coming back to investing after having waited 5 years. The demographics of the US are changing, slowly. The average age of a US citizen is closer to 40 than 30. This can be positive for companies that innovate new, useful products, yet can be deleterious to innovation. To supplement my expected innovation drought is the looming education bubble: "The credit-driven higher education bubble of the past several decades has left legions of students deep in debt without improving their job prospects."- Glenn Reynolds Link There needs to be a structural change to the, hidden, education crisis. Perhaps online education is filling that void? The author is incredibly focused on education. Smart kids mean better companies, more innovation, increased consumption, and finally, in the extremely long term, increased equity prices. Also, with the changing demographics the healthcare should have, at least, several tears of hearty growth.

Gold is at lows, equity’s are at highs, 10y yields are around 3%, market volatility is becoming more and more pent up, waiting to explode as markets rise ever higher. (Note: this was written in mid-January) Volatility breed’s opportunity, opening up trades that were once crowded, yet the investments, is fundamentally unchanged. International investors are the most upbeat about the global economy than at any time in almost five years, buoyed by the U.S.-led revival of industrial nations, according to the Bloomberg Global Poll. Link Another catalyst to equity markets is that the unemployment rate continues to, steadily, drop. Also, a white-collar wages are set to rise which implies that “unskilled” workers could augment the wealth of their bosses, improve sales and permit investors (traditionally white-collar workers) to, either start investing again, or make; larger purchases in the market. Another catalyst for companies and therefore equities is the INCREASING rate of technological advancements: “Something very, very big happened over the last decade. It is being felt in every job, factory and school. My own shorthand is that the world went from “connected to hyper-connected” and, as a result, average is over, because employers now have so much easier, cheaper access to above-average software, automation and cheap genius from abroad. Brynjolfsson and McAfee, both at M.I.T., offer a more detailed explanation: We are at the start of the Second Machine Age.” Suddenly, the speed and slope of improvement, they argue, gets very fast and steep. Link Interest rates WILL rise, the economy is healing and extremely accommodative rates are unsustainable if the population wants the government to grow, or benefit, from he economic expansion. “The debt overhang has been greatly reduced, monetary policy has, and will, stay incredibly loose, to speed up global circulation of capital.” Some non-investors may indirectly benefit from an up market. For example, a pension recipient may be less likely to face benefit cuts thanks to strong returns by a pension fund. A phenomenal past year in the stock market encourages wealthy consumers to spend more, which stimulates the economy. That is hoping that the jobless rate continues to fall. A surprisingly weak December jobs report suggests the optimism got ahead of itself. The Labor Department reported today that employers added just 74,000 jobs in December from November, less than half economists’ expectations of about 200,000. Link

Despite the tepid (but still positive) job numbers in the last month of 2013: what the quote fails to mention is that the job gains made in the 11 other months have a positive effect on the economy, increased consumption, circulation, and confidence. Along with increased hiring, trade domestic, and international has also picked up. Technically we have forfeited our, honest, trade numbers to China, However, although China is clearly in the lead, they still report inflated numbers. Curious. China Customs, everyone agrees, counted a substantial number of fictitious export transactions last year. Even with China reporting their trade numbers in an extremely optimistic manner. Link Although with these factitious trade numbers, the global economy is set to expand in 2014, led by the US and China. It is impossible to time a pullback. The only thing to hope for is that it is not so severe that it takes out new market participants. A mentor of mine said: “this is not a trading market, rather, it is a long time-horizon market.” Which bolsters the point made earlier in the piece, fundamental, rather than top-down analysis is what will drive returns in this market. For this year expect, again, equities to rise, perhaps buoyed by employment, housing and trade.

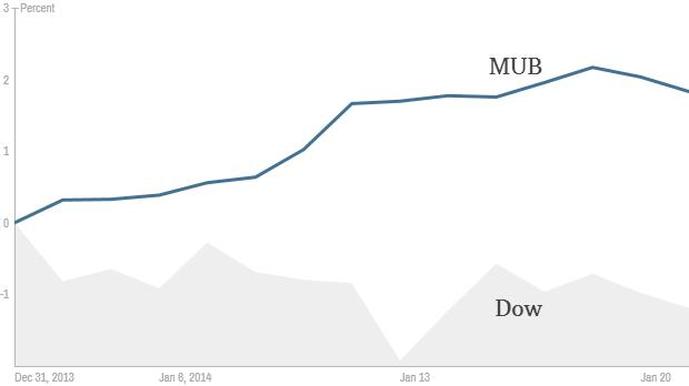

Bonds v stocks this year. (excuse the hard to see stock performance line, “DOW”).

Janet Yellen (the new FED chairwoman) doesn’t need to worry about when to remove stimulus, instead she has the perhaps more daunting task of retightening (increasing interest rates). Potentially even more detrimental than when “tapering” was announced. The markets, and businesses have grown accustomed to borrowing money for virtually no rate. Hoping the economy strengthens enough so that rates may actually rise, and the government actually make income on their loans. This (long term) might be a boon for the broad equity indices.

Expect around 4% growth, a much faster rate than what we’ve grown accustomed to, except last year. There does not seem to be too much (irregular) political noise. All positive factors for this years market. While pent-up buying does not seem too apparent, as that was clearly apparent in 2013, what might be the theme this year is that “retail” investors might come back into the market place. As well as increased investment in once shunned markets. Europe will (and is currently) exit recession, with the peripheral economies benefiting from the strongest relative improvement in growth prospects. Meanwhile, 3% annual GDP growth is no longer out of reach for the United States. And emerging economies will be anchored by China’s slower but still-robust 7% annual growth. Link

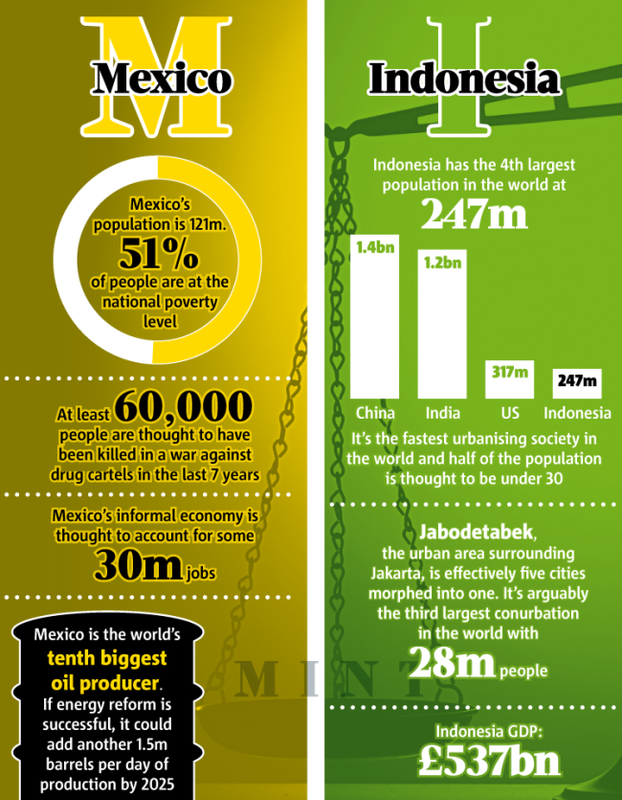

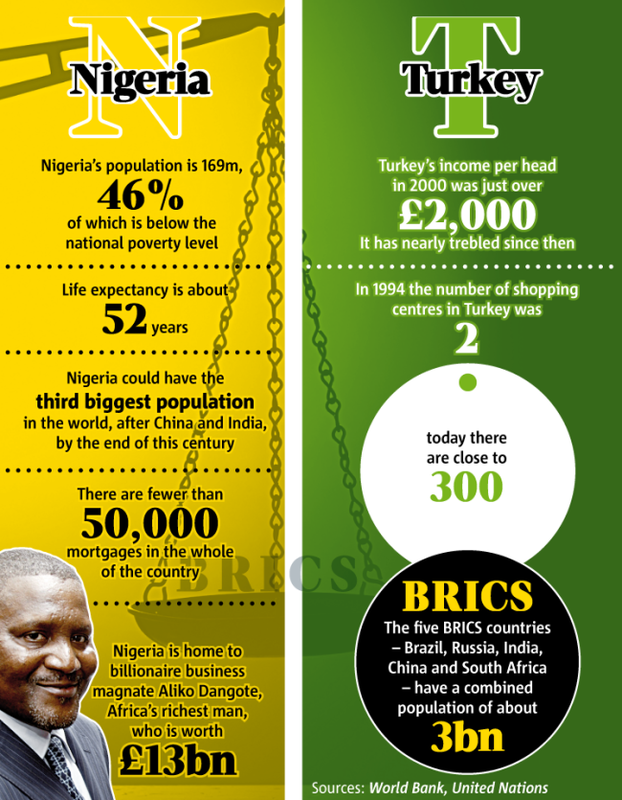

The latest investment acronym fad has arrived, MINT (Mexico, Indonesia, Nigeria, Turkey). These countries do offer attractive investment opportunities, perhaps it would be wise to allocate small portion of your portfolio to this new group. The performance of the MINT group for the beginning of 2014 has been much stronger than the S&P, also the performance should increase since all countries in this group have a clear economic advantage, one, shared, advantage is that each country on the list shares a growing class of young-adults, which should be a windfall for the consumption and all the secondary and tertiary factors that contribute to that: Mexico: For one the average age is below 30. The energy sector of Mexico is a huge benefit to the growth of the county. There is a definite abundance of sunshine in the state and Mexico is steadily increasing its energy output. Another positive attribute, as mentioned before, is the average age, which is below 30 years old. The age might not seem like a huge talking point, but consider how much consumption, especially a citizen in a country between 1) the second largest economy in the world (we forfeited that title to China’s, fishy trade numbers) and 2) the continent of many upcoming mass consumers (South America – home of Brazil). Mexico has boosted exports to the US as well the country has introduced a host of new economic reforms to fully capture the revenues derived off the increased exports. Finally, the location is quite fortuitous. Located between the world’s second largest economy and a major trading partner with Brazil (remember the BRIC acronym?), also Mexico has a solid trade partnership with China, which should be a major benefit as the Chinese population moves towards consumption. Indonesia: The majority of consumes are under the age of 25, unbelievably. The automobile industry, and all the industries that directly benefit, will likely see a large increase in business since Indonesians are commuting less and less on bike and more by car. Nigeria: While the content of Africa has been over looked for investment, it may be time to rethink that investment trait. With the rise of the youth population (again), the disposable income is surely set rise, which benefits a litany of industries. As one of the sole investment countries (Kenya being the other) the likely coming increase of investment will surely benefit the country, by increased investment in economic staples, those companies will likely, increase wages and buy equipment and material from other smaller Nigerian suppliers. All these factors make an extremely attractive investment climate in Nigeria. Turkey: This European country is currently in the process of sorting out its political issues. Turkey, which still uses the Turkish Lira, not the Euro, has faced significant declines in its currency; the declines will most likely be a win for all the exporters of Turkey. Also, the country has the unique fortune of being on two continents (Europe & Asia), which will definitely be a major shipping hub as global trade increases.  With Gold prices still falling (but expected to come back into favor in q3/4 of this year), housing already well-into its bull market, and bonds will probably not made any meaningful returns this year, equities will still be a place for investors to park money. Equities already had a stupendous rise in 2013, but the remainder of this year should see an equity rise due to, investors coming off the sidelines, the domino effects of last years rally and the infrastructure spending that Barak Obama has pledged to invest in in his second term.

For this year expect much slower growth (but growth, nonetheless), a continual improvement of the jobs picture, and increased global trade.The broad equity index, the S&P is expected to rise but no more than 10-15%, the wait for fixed income might be another year before we see any meaningful returns, physical commodities. Gold namely, will have to wait another 6 months at most, hopefully.What Bernake needs to realize is that his maintenance of stimulus for so long was keeping citizens invested in fixed income to avoid anticipated inflation. A good place to focus on to avoid the noise domestically would be the aforementioned MINT counties, however those counties host their own domestic issues. |

Archives

August 2014

Categories |

RSS Feed

RSS Feed