|

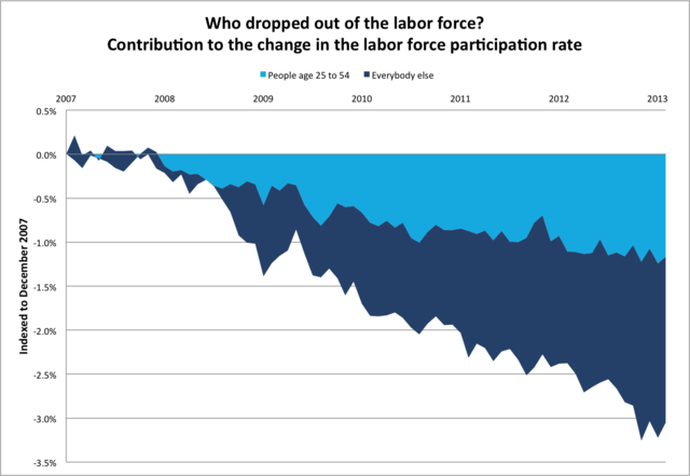

The current market environment yields a difficult-to-digest entry point. On one hand a majority of solid, stable, and secure “blue-chip” companies look to be trading at incredible discounts, on the other hand an investor would surely not want to get burned entering the stock market in the midst of a current pullback. Also incredible-momentum stocks (TSLA, NFLX, FB) are seriously waning. The best option is to not trade in this environment, it seems like the “froth” is being taken out. This is a good thing for long-term investor. A bad sign to compound the difficult entry point dilemma (of many bad signs) is that the employment to population ratio is normalizing. This ratio is normalizing because of the growing number of long-term unemployed. The ratio was skewed very badly during the great recession. This is worrisome and indicative of a structural shift. However, a contrary trend is emerging in an age-range of the population: Hiring over the past 12 months has outpaced population growth. More workers in the prime 25- to 54-year-old age group are finding jobs. The winter freeze was less destructive to hiring than had been assumed. Layoffs have declined since February. And an increase in hours worked suggest that incomes will rise. Link Also, unemployment claims are threatening to fall even lower, it MIGHT be from increased hiring or (more likely) frustrated unemployed, working-age citizens are collectively saying “sour grapes,” and willingly leaving or dropping off the reports due to length of unemployment. Despite, the relatively recent trend the economy was adding MORE people to the labor force than people leaving. Now getting a clean unemployment number is tricky, because many youths that have never entered the labor-force but are looking for employment cannot be counted.

To augment the hiring issues, through less options being available, is that ultra-discount stores like Family Dollar were hurt especially hard during the winter slowdown. Strangely, these types of stores outperform in tough economic environments. In difficult economic environments, ultra-discount stores perform very well since a majority of consumers are looking to cut corners on day-to-day expenses. However, in economic up-cycles (such as this one) those stores perform poorly, this recovery has a greater amount of structural issues so the current recovery has a lower slope than previous recoveries, this is the new normal. It does seem like consumers (who can) are spending more per holiday. What would be interesting to see, is if the rate of consumer spending per holiday has kept up or outpaced inflation. “[…]Yet Americans are on track to spend $15.9 billion on the holiday this year, according to the National Retail Federation. The average consumer (age 18 or older) who celebrates the holiday says she plans to spend an average of $137.46, up 42 percent from a decade ago. (Yes, these surveys of what consumers intend to do are notoriously inaccurate in terms of dollar figures, but they do give insight into actual spending trends.)” Link This is a positive trend. Slowly, well-off consumers will start to spend year-round. The increased profits will translate to larger pay for managers, the in turn will, (likely) reimburse their employees more, their employees will follow the same pattern, not as quickly, of course. This is essentially trickle down economics. With more and more people spending more on holiday shopping, this will eventually flow through to earnings. Equities are amid an earnings season right now, towards the end of this earnings period, at the very beginning of this period, the earnings were distorted by a lack of consumer traffic, blamed on the weather. There has been activity, and definitely buying in the IPO (Initial Public Offering) spectrum. Be cautious IF investing in an IPO. If investing betting (currently) in an IPO, look for a metric called “monetization.” Monetization means the strategy in place for the firm to make money, or, monetize their product offering. This metric should be closely watched for fledgling tech startups, they could have a major cash inflow from one large buyer, yet have little cash flow the following quarter. A country that has certainly had a great deal of activity, as well as a rash of Tech IPO’s is China. Currently, there exist fears that the Chinese boom may be ending.While China has undoubtedly served as a strong global economic locomotive, especially in the aftermath of the 2008 global financial crisis, expectations are for this role to diminish going forward. More of the heavy lifting is expected to be borne by the U.S. and Europe -- and indeed, needs to be borne by those economic powerhouses. That shift will optimally occur in the content of a proper rebalancing of global growth engines and an orderly, gradual normalization of experimental monetary policies.

As said in the quote, China has served as a robust economic growth engine, going forward, however, it will, most likely, slow its pace of expansion, as there is a shift from production to consumption. Eventually, the country supplying China will likely have a robust growth period, and the cycle continues. Buying here, with the market at depressed levels, makes sense. Buying “story” stocks (FB, TWTR, etc) is probably not too, considering this is PROBABLY the back end of the pullback. Snapping up cheaper (now), blue-chip (high-quality), dividend-paying stocks would be an excellent way to take advantage of high-quality names. There was not really a good opportunity last year, however, barring a catastrophic fall, high-quality names mat not be at this price level for long. After a few rocky days for stocks, it's time to set aside fear and buy growth companies on the cheap, says T. Rowe Price portfolio manager Josh Spencer. Link Another point of concern emanating from China is the fact that their property market is heating up very quickly. This may predicate a global growth slowdown, hopefully the MINT countries can help with the growth reduction, and lessen the blow to growth. “The far flung smaller cities account for almost 70% of all home sales, according to Japanese brokerage Nomura.” A potential issue with the dislocation of home sales, is that most sales are occurring away from production hubs, meaning a shift from export driven money may be well underway. Since a slowdown would surely affect citizens (the driving consumption behind GDP), the overheating of the property market would definitely harm the global recovery. Since China being an economic superpower is relatively young perhaps there is not ample data to indicate China will pull down the global economy. That might be too optimistic. Many, systemically important, economies are tied to health of the Chinese economy as well. This could bode poorly for global growth, so best to lighten Chinese allocation, and pick up cheaper high-quality, dividend-paying, names. The Chinese economy is indeed globally important, and to belie what was said in the last paragraph; China is a systemically important economy. That economy provides the fuel for growth for many economies. What is interesting is the fact that many well-off oriental citizens have developed a penchant for European goods. Perhaps their current shift towards consumption will boost exports from Europe and aid the ongoing economic calamity there.

0 Comments

The markets (SPX, DJIA, NASDAQ) is experiencing yet another pullback. Sadly this pullback is most likely clobbering investors that have only recently come off the sidelines. That is two (retracements) this year! With the lack of news flow (no news is good news) and, the increase of people joining the workforce, as well as the increase of hiring, all points to a gradual pick up. The equity markets have increased AHEAD of positive economic news. The unemployment rate might be falling, NOT because of increased hiring, but rather people dropping out of the workforce, the so-‐called “stealth” unemployed. Hiring IS taking place, just not at as vigorous levels as the data would indicate. To deal with this the FED is, clearly, backing away from its previously set 6.5% unemployment mandate, the mandate was set to begin raising borrowing rates. Keeping the federal funds window open at such low borrowing levels could be inflating another bubble. “We know we’re not close to full employment, not close to an employment level consistent with our mandate, and unless inflation were a significant concern, we wouldn’t dream of raising the federal funds rate target,” Chair Janet Yellen said. Hopefully providing the traction that equities are looking for, before continuing last years (slower) rise. “The economy is getting better, and it’s likely the softer patch we’re seeing is weather related,” Josh Feinman, the New York-‐based global chief economist for Deutsche Asset & Wealth Management and a former Fed senior economist,  To enhance these gains, is that the US equity markets have undergone a massive price increase, OUTpacing economic improvements. This has definitely been augmented by the US federal reserves willingness to move goalposts (set for borrowing-‐rate hikes) of unemployment, down from 6.5% (to a level we still do not know. The unemployment rate MAY spike up soon due to “long-‐term” unemployed coming back into the labor force (thus destroying the chance of rate hikes, AND extending the rally). “The Federal Reserve gave itself room to keep borrowing costs low at least until next year by dropping a linkage between the benchmark interest rate and a specific level of unemployment” “...and unless inflation were a significant concern... In deciding how long to keep rates low, the committee will look at a“wide range of information,” including labor market conditions, inflation expectations and financial markets, she said. The Fed also reduced the monthly pace of bond purchases by $10 billion, to $55 billion....” Thankfully, deficits on the federal and state level are shrinking. Also, the US is on the road to energy independence (no more wars over oil {essentially}, this MIGHT be injurious for defense and military contractors). Ideally, those sectors would shrink, so such a large portion of the national budget is freed-‐up. Having a larger portion of the national budget available would surely boost GDP, through economic-‐advancing projects such as: infrastructure, poverty spending, increasing of min. wage (increasing consumption) etc.  The US economy will most likely not be able to return to > 3% GDP growth rates. The confluence of hiring NOT taking off and the shift from production to consumption in China make for a bleak outlook. Hopefully, confirming the old adage, or theory, that transportation stocks usually predicate a run-‐up in equity prices, the transportation index has rallied and closed on Monday at an all time high. Defying the pullback most equity markets are facing. Valuations are high, however, they are nowhere near their absolute peak, right before the bursting of the 1999/2000 bubble. The Obama administration has set forth with a plan to buy 1 trillion of “troubled”assets from banks. This, risky, move by the US government should help to unfreeze credit markets. This will help by allowing banks to have a quota of “risky” loans emptied, which should definitely help the flow of capital. Since he credit markets are near frozen for citizen Another positive measure directly benefitting the middle class; job gains have been made across the spectrum of industry and job-‐level. This should enhance the earnings of the company they work for and therefore increase the performance bonuses of their managers. Managers usually are invested rather than entry-‐level employees. However, hourly wages fell in March, this COULD mean that hourly employees are being promoted to full time, more likely is that hourly-‐level employees are being let go.  With a 192,000 decrease in unemployment, the rate is dropping, slowly. This data indicate that the US economy will return to full employment (not 0 unemployed, rather, unemployment rate at <6.4%). The US economy may take much longer to reach full employment since, the job market grows by ~3% every year and, the US economy suffered 3 years of no growth whatsoever, so that mean the economy has a good deal to make up before it begins to reach “full” employment.

Theoretically, ”full” employment is just below 5%, compounding this challenging measure to reach is that; the population is ALWAYS changing, albeit not by much and the changes are certainly not made by increases or decreases in working-‐age citizens. Rather population growth (also slowing) is a key measure to watch. Jobs, as it must be apparent now, are perhaps the key to economic growth. With in increased jobs the US enjoys a litany of other windfalls. Increased consumption, leading to more jobs. It’s really a self-‐fulfilling cycle. Insider selling (executives selling stock in their own company, a bearish sign) has reached a high. Yet, insider selling of certain, but important industries has NOT reached a high. Those industries are: financials, energy and basic industrials. Ill go through each industry and explain why this may be undue pessimism: Financials: An industry, which relies heavily on trading profits, trading profits come in up OR down markets, however, in down markets profits are limited (cannot derive profits after 0). In up markets profits are unlimited. Energy: If more companies (particularly manufacturing) need to operate more/longer, forcibly those companies will need more energy. This, I believe is an important, indicative, industry. Basic Industrials: It would seem like basic industrials go into production of almost everything. If that industry in going well, like energy, it would seem like production, thus (hopefully) the economy is doing well. Five years into the bull market, Byron Wien doesn't see a top in sight. In fact, the vice chairman of Blackstone Advisory Partners says that there's still plenty of time to buy stocks. I think the market's going to flutter around a little bit here in the first half, but I think it's going to be relatively strong in the second half, and I think this year is going to end up surprising people favorably," Wien said on CNBC.  A trader in VIX has, again, bought a huge quantity of VIX call options in hopes that the index rallies (not good)between now and May, (VIX, as I explained in the second piece, increases based on the “noise” around the general movement of an index, in this case the SPX.) VIX has rallied over the past week, based on fears that the market is reaching overbought territory or is in a “bubble,” and the geopolitical events in Ukraine/Russia.Markets do seem a bit “frothy,” however, the author thinks that the only thing that needs to happen, is the fact that thousands of large brick & mortar retailers are closing stores. That action foretells deflation, with no consumers to buy cheapened goods (jobs are being cut) countries might drag the global economy down, starting with the inability to purchase goods here.Goods that other countries produce. Decoupling (when other countries do not need to rely on the US to sustain their growth, it can come from increased domestic production/sales {preferable}, or from an international sales pickup).China and the other BRIC countries are beginning to not rely so heavily on the US for growth. This can be a good thing, or a bad thing, we (the US) suffer by a decreased velocity of trade between the decoupling countries, but it’s a positive because, an increased, worldwide, velocity of money has a positive economic effect for the global economy.

A childless economy is also detrimental to global growth, once guaranteed consumers will slowly dwindle down and harm the growth prospects of OTHER countries. China is driving down exchange rates in an effort to keep their factories pumping out products for US consumers. Clearly, If China continues they will have fewer consumers to sell to. As said in the third piece, all MINT markets boast a young and increasingly educated younger population. Not immediately, in the long term, however, it might be wise to SLOWLY reduce domestic exposure. This is a very slow moving theme, Perhaps the US can increase baby “production” and this demographic disaster can be avoided. Equities do seem like they are trying to find traction before continuing last years rise, albeit at a much muted pace. Economic indicators all point towards growth, and the indicators foretell an eventual boost in spending and thus earnings. Also, companies are almost done working through their over-production (as a result of consumers not consuming at their regular pace), once their inventory reaches normalized levels, US production can ramp up again.  In an effort to find directionality,worldwide markets arevery active next month could be very indicative of the direction the global economy is headed. Many major indices, all over the world, are trading at or close to points that, if crossed in the wrong direction could mean a great deal for that countries economy. The future movement in equity prices are definitely no reason to be completely in, or completely out of equities or the markets. The future movement is just a small sample of the entire financial picture.

A much longer, structural change, is that the US GDP has been falling, since its peak in 1969. The author has many beliefs as to why, belief is that the rise of technology (you can now order anything from the internet) has imposed complacency on the population as a whole. Why go to the store if you can get the same product delivered to you door? Thankfully entrepreneurs are hard at work coming up with new ways to try and make foot-traffic fall more slowly. Thankfully is does seem, from looking at holiday shopping bonanzas, that a foot-traffic fall off is a long way off. There tensions surrounding Ukraine are easing. With those tensions out of the way, stocks rallied when Putin called his troops back from their military exercise. The spate of soft data hasn't budged his strong outlook for the economy, St. Louis Fed chief tells CNBC. Formerly a fence-sitter leaning hawkish, Bullard titled dovish late last year - constantly reminding too-low inflation was just as much of a worry as what economic growth was doing. He's about-faced in 2014, now leaning hawkish and taking every opportunity to tell people it's probably the weather causing the recent slowdown. Moving away from geopolitical events, the prices of homes may increase, especially following the excellent year we had last year. Although the increase in prices may not be as dramatic as last year, do expect a mediocre rise in prices. The land on which homes are built also plays a large role in housing prices. With the average age of the US population slowly creeping up (more on that later) housing prices may face a lower slope in the long-term. This play very well into was mentioned in the first paper: perhaps private equity and hedge funds are buying many residences (there is record of increased buying) to eventually create a new security based on renal payment streams. As mentioned before but certainly worth repeating; is that President Obama has allotted congress more money to fix and build infrastructure, as needed. This seemingly routine move by Obama has deep implications for our growth, and the growth of international companies. Improved infrastructure will not only make us safer, but also facilitate the ease of flow for goods, domestic and, more importantly, abroad.

As this was being written, Putin called back his troops from their “military exercise.“ There is definite interest in recapturing former soviet states, however, Russia is too deeply in debt and the value of the Ruble (obviously the main trading tool) has increase dramatically, it is unclear if Putin plans to pay off the debt overhang or purchase equipment f or an upcoming invasion. Watching the actions Putin takes with the increased value of the currency is crucial to not only determining the fate of Yugoslavia, but also determining an increase of orders for suppliers. In keeping with Eurozone actions, the ECB will be conducting a stress test (in stress tests the government authorities, simulate a massive withdrawal of captal to ensure that the bank can handle a liquidly withdrawal and function [make/pay loans, deposits etc..]). The ECB hopes to restore market confidence in the financial condition of eurozone banks by conducting a "comprehensive assessment," including a stress test, of 130 of the largest ones, representing 85 percent of eurozone banking assets. The strong ones will be certified, while the weak ones will be obliged to recapitalize themselves. Link

The US economy added ~175k new jobs, yet the unemployment rate still jumped 10 basis points. Why? The author thinks that with the unemployment rate steadily dropping, this perhaps giving more hope to jobless individuals. With more motivated individuals there are most likely individuals who are “long term” unemployed thus the increased number of people in the sample size increases. Possibly 175k more people entered the statics, thus skewing the data. The brings up another point, if the unemployment rate can rise when more jobs were created than forecast, that is an ominous sign for the unemployment rate. “As for declining labor force participation? It's a secular trend, not cyclical, he says.” A pullback from the current rate of economic growth is highly unlikely. Despite the overt upbeat tone and nature of this piece, there could be another pullback brewing. Many Chinese companies are deeply in debt, and the first corporate default has just occurred, and there is, for the first time, no government support for them. Also, the equity markets keep breaking new highs, as they should during a unrestrained growth period. “Many regular columnists speak about how the stock market is poised for a drop, and that could very well happen, however, as mentioned above it really does seem like fundamental indicators are pointing towards a continued improvement. ”Political risk expert Ian Bremmer from Eurasia Group is calling this crisis "the most seismic geopolitical events since 9/11."

A, needed, pullback is gripping the equity markets. The SPX has lost roughly 3.5% of its value; accordingly, consumer confidence has slipped. “Strong household spending and robust exports kept the U.S. economy on solid ground in the fourth quarter, but stagnant wages could chip away some of the momentum in early 2014." January, is down almost 6% MTD and YTD. There is a known pattern; the year follows the first month of that years returns trend (body follows head, right?). The author thinks that given the positive data flow at the end of 2013, means that there is little chance that the equity markets in 2014 end negative. There is acceleration in employment, which means acceleration in consumption, money velocity etc.… Although it is possible for the year to end poorly (2014), the economy would to need grow at a blistering pace of < 3.2% for any reported number exceed the great growth we had in q3 of 2013.

This retracement is linked to emerging market counties, however, the underlying investment thesis has not changed. The countries did not change their trade partners nor did they reduce their rate of consumption. Rather, the currencies have decreased in value, their fundamentals have not changed. This could be a negative indicator, domestically if their currencies stay at this level, a depressed currency means that we, or other countries cannot sell tools they need to grow, thereby hurting our growth and growth of other countries. That could pose a serious problem for the global economy. Generally, global GDP is picking up. The auto industry is leading the way (probably led by China); building orders, construction and airlines (to name a few, but economically important) are seeing an increase in order flow/completed orders. Hoping we are experiencing a brief retracement, led by currencies of emerging markets. Optimistically, the trend will pick back up soon. With positive data coming from most countries, consequentially, order flow should increase among all industries, shipping products to various countries that have ordered them. This, in return should boost global gdp. The IMF last week forecast the emerging markets would grow at 5.1% this year, compared with 4.7% in 2013. China is expected to grow at 7.7% this year — hardly a crisis by anyone’s standards. Even hard-hit Turkey is expected to expand by 4% over the next twelve months. Too optimistic? Not really. The euro-zone has stabilized, at least for the time being, which will help Eastern Europe and Russia and Turkey. The U.S. is growing faster than at any time since the crash, which will help South America. So long as China can stay on course, it will carry on lifting the whole of Asia. Emerging Africa remains one of the fastest-growing regions in the world, and shows few signs of slowing down. -- Growth in emerging markets is accelerating, not slowing down. The recent selloff is blamed on EM countries, however, its completely normal to have an unprovoked sell off after 16 months of extraordinary returns. Link

Although their respective currencies have cheapened in the MINTS countries, their YoY GDP growth (year over year) of the South American, southern Africa, and southern Asian countries is impressive. The economy in Mexico, is growing very quickly. What could be a potential problematic point is that the Mexican Peso is highly correlated to South American currencies. This could be a problem for two reasons: 1) the recent retracement is blamed on currencies which is a major concern for growth due to the second reason, 2) without a strong currency they may not be able to properly or effectively develop their oil fields, those are a major key for growth. A large contributor to the Mexican economy is the economy of the US. Everyone knows that the move by the Fed to back off from asset purchases, and eventually to raise interest rates, will have major economic impacts here and abroad. The problem is in predicting what those will be and, especially, the magnitude of the effects. One source of uncertainty is the transition from a Bernanke Fed to a Yellen Fed, but it would be easy to over-estimate the importance of that factor. In reality, there is quite of lot of common ground between the outgoing and incoming Chairs. The more important issues revolve around the fact that we are simply in uncharted territory. The sturdy increase in demand should put the economy on a stronger growth path this year. However, anemic wage growth could take some edge off consumer spending early in the year. Given everything, the author thinks that this year should be in the black for equities. Going from a +30% year to a negative year, sequentially, is rather daft. As well, consumer spending rose at the fastest pace in 3 years despite the government, coincidentally (tapering) or reducing spending at the same time. The positive data flow is certainly laying the groundwork necessary for 2014 to be a positive year, again, not as great a rise as 2013 but still belying the impression that January has given the market.

The equity market seems to have lost steam (but hopefully not momentum) with the turn of the year, and especially in the second half of the month. Equities seem to be fair-valued—in this type of market fundamental analysis, AND having a longer time horizon for expected profits are keys to excess returns. With the recent pullback, it should create buying opportunities and will lure investors back into the market. Whereas all of 2013, especially the last quarter of 2012, was a “shooting gallery,” when it seemed like almost any equity you poured money into yielded awesome gains. This year it would be wise to look at historical price charts, and also look if order flow is increasing, which clearly points at higher net income. Earnings momentum, undoubtedly is an advantage to, all this coincides with the suggestion that fundamental analysis should be core to the equity selection process. Earnings momentum ended last year on a very positive note, q1 earnings should confirm reported earnings. A “great rotation” from equities into fixed income could come this year, as said GDP growth follows equity returns and equity returns. Moreover, with the increasing average age of the population, there is a high chance this shift could happen within >10 years. It would be shrewd to look for counties that this shift will happen sooner rather than later.

A pullback after the relentless rise we experienced , unbroken for <12 months), is more than needed, corrections serve two purposes. They help to slowly restore faith in the equity market by: pulling investors who remained on the sidelines after the tremendous run of last year into the market and with more investors participating the swing to positive territory could be much more dramatic. The beginnings of this trend were apparent at the beginning of this year, likely due to the volatile beginning of the year. Also, it gives a chance for investors already in the market to rebalance or adjust weightings without too big of a hit on year-to-date returns. Thankfully this correction happened towards the beginning of the year. Pent-up profit taking was apparent in the beginning of this year; many investors were probably delaying profit taking for tax reasons. Such tax strategies are positive for personal wealth, but deleterious for the market and popular equities (making them more attractive). The volatility of the beginning of the year is also a positive for investors coming off the sidelines, and coming back to investing after having waited 5 years. The demographics of the US are changing, slowly. The average age of a US citizen is closer to 40 than 30. This can be positive for companies that innovate new, useful products, yet can be deleterious to innovation. To supplement my expected innovation drought is the looming education bubble: "The credit-driven higher education bubble of the past several decades has left legions of students deep in debt without improving their job prospects."- Glenn Reynolds Link There needs to be a structural change to the, hidden, education crisis. Perhaps online education is filling that void? The author is incredibly focused on education. Smart kids mean better companies, more innovation, increased consumption, and finally, in the extremely long term, increased equity prices. Also, with the changing demographics the healthcare should have, at least, several tears of hearty growth.

Gold is at lows, equity’s are at highs, 10y yields are around 3%, market volatility is becoming more and more pent up, waiting to explode as markets rise ever higher. (Note: this was written in mid-January) Volatility breed’s opportunity, opening up trades that were once crowded, yet the investments, is fundamentally unchanged. International investors are the most upbeat about the global economy than at any time in almost five years, buoyed by the U.S.-led revival of industrial nations, according to the Bloomberg Global Poll. Link Another catalyst to equity markets is that the unemployment rate continues to, steadily, drop. Also, a white-collar wages are set to rise which implies that “unskilled” workers could augment the wealth of their bosses, improve sales and permit investors (traditionally white-collar workers) to, either start investing again, or make; larger purchases in the market. Another catalyst for companies and therefore equities is the INCREASING rate of technological advancements: “Something very, very big happened over the last decade. It is being felt in every job, factory and school. My own shorthand is that the world went from “connected to hyper-connected” and, as a result, average is over, because employers now have so much easier, cheaper access to above-average software, automation and cheap genius from abroad. Brynjolfsson and McAfee, both at M.I.T., offer a more detailed explanation: We are at the start of the Second Machine Age.” Suddenly, the speed and slope of improvement, they argue, gets very fast and steep. Link Interest rates WILL rise, the economy is healing and extremely accommodative rates are unsustainable if the population wants the government to grow, or benefit, from he economic expansion. “The debt overhang has been greatly reduced, monetary policy has, and will, stay incredibly loose, to speed up global circulation of capital.” Some non-investors may indirectly benefit from an up market. For example, a pension recipient may be less likely to face benefit cuts thanks to strong returns by a pension fund. A phenomenal past year in the stock market encourages wealthy consumers to spend more, which stimulates the economy. That is hoping that the jobless rate continues to fall. A surprisingly weak December jobs report suggests the optimism got ahead of itself. The Labor Department reported today that employers added just 74,000 jobs in December from November, less than half economists’ expectations of about 200,000. Link

Despite the tepid (but still positive) job numbers in the last month of 2013: what the quote fails to mention is that the job gains made in the 11 other months have a positive effect on the economy, increased consumption, circulation, and confidence. Along with increased hiring, trade domestic, and international has also picked up. Technically we have forfeited our, honest, trade numbers to China, However, although China is clearly in the lead, they still report inflated numbers. Curious. China Customs, everyone agrees, counted a substantial number of fictitious export transactions last year. Even with China reporting their trade numbers in an extremely optimistic manner. Link Although with these factitious trade numbers, the global economy is set to expand in 2014, led by the US and China. It is impossible to time a pullback. The only thing to hope for is that it is not so severe that it takes out new market participants. A mentor of mine said: “this is not a trading market, rather, it is a long time-horizon market.” Which bolsters the point made earlier in the piece, fundamental, rather than top-down analysis is what will drive returns in this market. For this year expect, again, equities to rise, perhaps buoyed by employment, housing and trade.

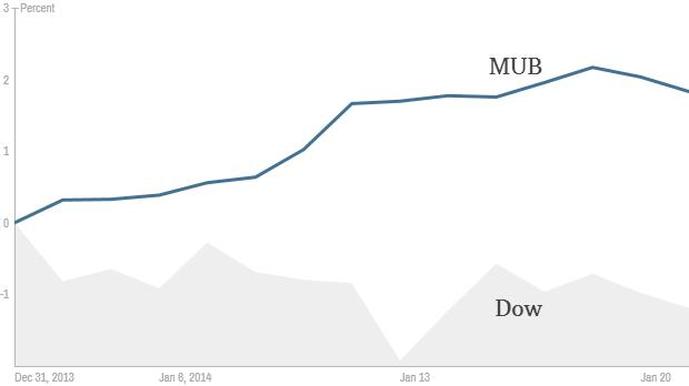

Bonds v stocks this year. (excuse the hard to see stock performance line, “DOW”).

Janet Yellen (the new FED chairwoman) doesn’t need to worry about when to remove stimulus, instead she has the perhaps more daunting task of retightening (increasing interest rates). Potentially even more detrimental than when “tapering” was announced. The markets, and businesses have grown accustomed to borrowing money for virtually no rate. Hoping the economy strengthens enough so that rates may actually rise, and the government actually make income on their loans. This (long term) might be a boon for the broad equity indices.

Expect around 4% growth, a much faster rate than what we’ve grown accustomed to, except last year. There does not seem to be too much (irregular) political noise. All positive factors for this years market. While pent-up buying does not seem too apparent, as that was clearly apparent in 2013, what might be the theme this year is that “retail” investors might come back into the market place. As well as increased investment in once shunned markets. Europe will (and is currently) exit recession, with the peripheral economies benefiting from the strongest relative improvement in growth prospects. Meanwhile, 3% annual GDP growth is no longer out of reach for the United States. And emerging economies will be anchored by China’s slower but still-robust 7% annual growth. Link

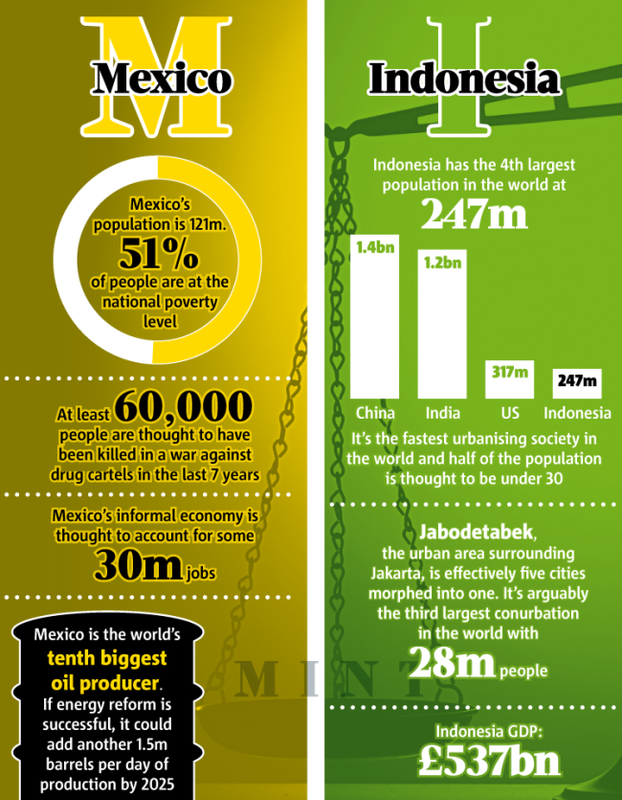

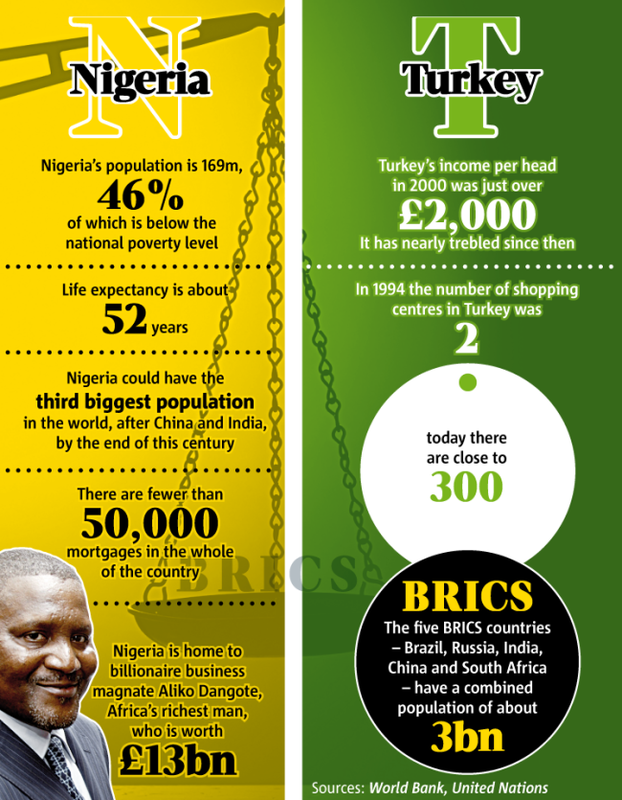

The latest investment acronym fad has arrived, MINT (Mexico, Indonesia, Nigeria, Turkey). These countries do offer attractive investment opportunities, perhaps it would be wise to allocate small portion of your portfolio to this new group. The performance of the MINT group for the beginning of 2014 has been much stronger than the S&P, also the performance should increase since all countries in this group have a clear economic advantage, one, shared, advantage is that each country on the list shares a growing class of young-adults, which should be a windfall for the consumption and all the secondary and tertiary factors that contribute to that: Mexico: For one the average age is below 30. The energy sector of Mexico is a huge benefit to the growth of the county. There is a definite abundance of sunshine in the state and Mexico is steadily increasing its energy output. Another positive attribute, as mentioned before, is the average age, which is below 30 years old. The age might not seem like a huge talking point, but consider how much consumption, especially a citizen in a country between 1) the second largest economy in the world (we forfeited that title to China’s, fishy trade numbers) and 2) the continent of many upcoming mass consumers (South America – home of Brazil). Mexico has boosted exports to the US as well the country has introduced a host of new economic reforms to fully capture the revenues derived off the increased exports. Finally, the location is quite fortuitous. Located between the world’s second largest economy and a major trading partner with Brazil (remember the BRIC acronym?), also Mexico has a solid trade partnership with China, which should be a major benefit as the Chinese population moves towards consumption. Indonesia: The majority of consumes are under the age of 25, unbelievably. The automobile industry, and all the industries that directly benefit, will likely see a large increase in business since Indonesians are commuting less and less on bike and more by car. Nigeria: While the content of Africa has been over looked for investment, it may be time to rethink that investment trait. With the rise of the youth population (again), the disposable income is surely set rise, which benefits a litany of industries. As one of the sole investment countries (Kenya being the other) the likely coming increase of investment will surely benefit the country, by increased investment in economic staples, those companies will likely, increase wages and buy equipment and material from other smaller Nigerian suppliers. All these factors make an extremely attractive investment climate in Nigeria. Turkey: This European country is currently in the process of sorting out its political issues. Turkey, which still uses the Turkish Lira, not the Euro, has faced significant declines in its currency; the declines will most likely be a win for all the exporters of Turkey. Also, the country has the unique fortune of being on two continents (Europe & Asia), which will definitely be a major shipping hub as global trade increases.  With Gold prices still falling (but expected to come back into favor in q3/4 of this year), housing already well-into its bull market, and bonds will probably not made any meaningful returns this year, equities will still be a place for investors to park money. Equities already had a stupendous rise in 2013, but the remainder of this year should see an equity rise due to, investors coming off the sidelines, the domino effects of last years rally and the infrastructure spending that Barak Obama has pledged to invest in in his second term.

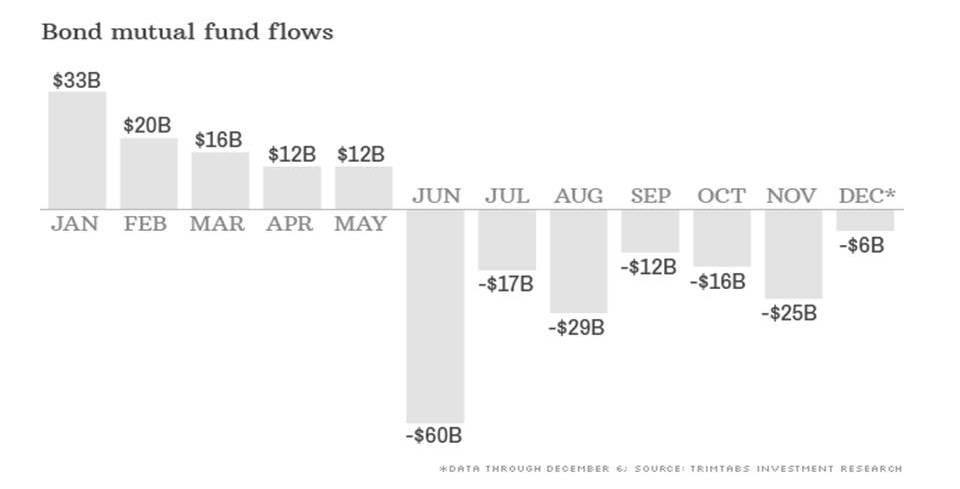

For this year expect much slower growth (but growth, nonetheless), a continual improvement of the jobs picture, and increased global trade.The broad equity index, the S&P is expected to rise but no more than 10-15%, the wait for fixed income might be another year before we see any meaningful returns, physical commodities. Gold namely, will have to wait another 6 months at most, hopefully.What Bernake needs to realize is that his maintenance of stimulus for so long was keeping citizens invested in fixed income to avoid anticipated inflation. A good place to focus on to avoid the noise domestically would be the aforementioned MINT counties, however those counties host their own domestic issues. It looks like larger investors are positioning for the upcoming reduction of federal support of buying open market securities. A trader, specifically one that trades VIX futures/options (VIX is a tradable volatility security, VIX increases in up OR down markets depending on “noise” around the general movement), has recently purchased over 4 million dollars of the future right to buy VIX at its December 12th price. This points, clearly, towards increased volatility. With the equity markets at all-time highs, the economy has been expanding for 53 months, and payrolls have risen by nearly 7.5 million since February 2010. Volatility in the equity markets can only mean that there will be much larger moves on a trend going down, increased volatility is not welcome. However, these are option contracts, the trader (under his client or clients consent) can let the contracts expire with only the capital used to purchase the options lost. Conversely, the economic data points towards an ongoing economic growth period. Payrolls, hiring, confidence/optimism, and incomes are rising. Perhaps volatility could be ushered in by an anticipated fall in foot traffic of brick &mortar stores. The fall might be able to be predicted by the price movement of gasoline prices. The recent rise in gasoline prices may be a contributing factor to the rise in popularity of online retailers and slower holiday season shopping, on the ground. Look for holiday shopping figures, or Q4 figures, reported strictly by brick and mortar outlets, to be not as robust as anticipated. Despite my anticipated slower PHYSICAL goods consumption, I believe that given positive data flow we may see stronger reported sales by online retailers.  “I will make one prediction: The early forecast about holiday shopping will be wrong; the season will be better than worst expectations, perhaps not living up to the most optimistic ones.” Link Another contributing factor for a potential slowdown in Q4 GDP figures can be attributed to the government shutdown. Federal workers were not paid which means a litany of private services did not collect the anticipated level of revenues. Think buses to federal attractions that were not operating at normal capacity or even as simple as government attractions that were closed, the huge missing consumption of federal workers paid by the government, etc. As the author mentioned in the last article; the equity market is really a playground for well-heeled investors who can invest, and invest with size. Fixed income, which is what a majority of senior citizens invest with, in retirement, has not made any notable returns. The small-time, retail, investors are becoming more invested “the growing involvement of Main Street investors in the stock market just as we’re hitting all-time highs — a contrarian sign, if there ever was one.” Probably lured back to the market by incredible gains seen this year. Link If volatility does indeed return it would be opportune to buy fixed income, as bonds will certainly increase.Fixed income is a good place to safely be invested and hopefully make gains at the same time, bonds or any tangible asset.This is, of course, if the reduction in stimulus adds volatility. Further, bonds have had an extremely rough year, preventing investors currently in the market,to profit from another asset class (namely, equities) rising.  Chairman Bernake first mentioned a reduction in stimulus in May, as you can see the assets under management in fixed-income mutual funds have been consistently negative. Thankfully the unemployment rate drops every month. The unemployment rate below 6.5% should trigger an increase in the fed funds rate. This increase in the rate at which businesses borrow (to perform self-improvement tasks) money may constrict the growth of a stimulus-free equity market. However, in the December, 18th FOMC meeting chairman Bernake stipulated that:, the governmental window, which companies use to bridge short-term expenses, will stay at the current (extremely low) rate or 25 basis points (.25%). Also, the FED will be reducing stimulus by 10 bln/month, which seems like a nice, gradual, slope to remove this program. As mentioned in the previous piece, inflation could rear its head when tapering begins, expected inflation kills aggregate demand in anticipation of a lower real price. Businesses will likely invest more in hopes for growth, since they no longer rely on the FED for capital market buying, so look for increased CAPEX which leads to better or upgraded oil/utilities/telecom etc. which would ultimately increase the domestic infrastructure which would increase global trade. So, keeping the open market committee alive this long, may be harmful for global growth. Just as this was being written, the FED decided to reduce stimulus by $10 billion/month. However, they decided to keep the window from which businesses borrow money of at ¼ percent, the interest rate that SHOULD increase will remain pegged very low. That decision is likely done to increase CAPEX spending, a form of stretching stimulus  Finally, money managers are going on an end of year “spending spree.” The removal of stimulus is prodding investors to reaffirm the strength in businesses they thought was/is there. Money managers (a large majority of which have woefully trailed the broad equity market returns) are trying to not repeat the same mistake of being slightly invested at the beginning of the year. The remaining question is: how will the markets react then transition from Benjain Bernake to Janet Yellen. As a FED chairperson. The author has great confidence in a continuation of a rising equity market, well into next year. Not the pace or of the current rise, but certainly the direction. With all three major indices constantly breaking their all-time highs, and the current rally likely to be supported by a “Santa Claus bump” in demand, this all points to a growing net profit line.Also the increase or hiring should lead to more disposable income, which is a boon for manufacturers. All measures of economic performance are pointing up. Again, the rise this year was extraordinary, do not look for the same percentage increase next year, next year will probably, barring any major crisis, be a more tepid 10-15% year for equities. On December 12, the Census Bureau reported that retail sales rose a healthy .7 percent in November from October, and were up 4.7 percent from November 2012. So far this year, retail sales are up 4.3 percent from 2012. More people are working at slightly higher wages, and so they’ve got more fuel for consumption. Meanwhile, something else seems to have changed. Since the financial crisis, American consumers have been hacking down at their mountain of debt—through foreclosure and default, yes, but also through paying down credit cards, home equity lines, and credit cards, and by stopping themselves from taking on new debt. Generally, the amount of revolving debt (i.e. credit cards) is back to the level it was at in 2006. But this is changing. Earlier this month, the Fed reported that in October, revolving credit rose at a 7.5 percent annual rate. Americans are gingerly releveraging. (Matthew Boesler at Business Insider dubbed a chart showing this increase “the most important chart of 2013.”) That’s good news for consumption, so long as people can maintain their debts. And guess what? Debt service as a percentage of disposable income is at an extremely low level. Economy has been expanding for 53 months, and that payrolls have risen by nearly 7.5 million since February 2010. Link  |

Archives

August 2014

Categories |

RSS Feed

RSS Feed